Weltenergierat–Deutschland is the national member representing the Federal Republic of Germany at the World Energy Council. Its members include companies in the energy industry, associations, academic institutions and individuals. As a non-governmental, joint profit association, Weltenergierat-Deutschland is independent in its opinion. Its objective is to implement and disseminate key World Energy Council insights and knowledge in Germany, in particular, to bring the global and longer-term issues and needs of the energy and environmental policy to the attention of the national debate. To this purpose, it organises its own events and carries out its own studies.

Carsten Rolle, Secretary General of the German Member Committee of the World Energy Council since 2005, holds a PhD in economics from Münster University. After his studies, he managed the department for telecommunications and postal services at the Federation of German Industries (BDI) in Berlin. Since 2008 he has been the Managing Director of the Energy Policy department.

Maira Kusch is Head of Office at World Energy Council – Germany. From September 2020 to December 2021, she held the position of Senior Manager at WEC Germany. Before joining the World Energy Council network, Maira Kusch worked as Senior Consultant for energy, environment and mobility at the EPA European Berlin Brüssel Political Affairs GmbH, a strategic consultancy based in Berlin, and as Policy Advisor for Matthias Groote, MEP, in the Committee on the Environment of the European Parliament in Brussels and Strasbourg. She holds a Master’s degree in International Studies / Peace and Conflict Research and a Bachelor’s degree in European Studies. Maira is co-author of the book “Flüssiggas und BioLPG in der Energiewende” (“The Role of Liquefied Petroleum Gas and BioLPG in the Energy Transition”), published at VDE VERLAG, Berlin in 2020.

Energy in Germany

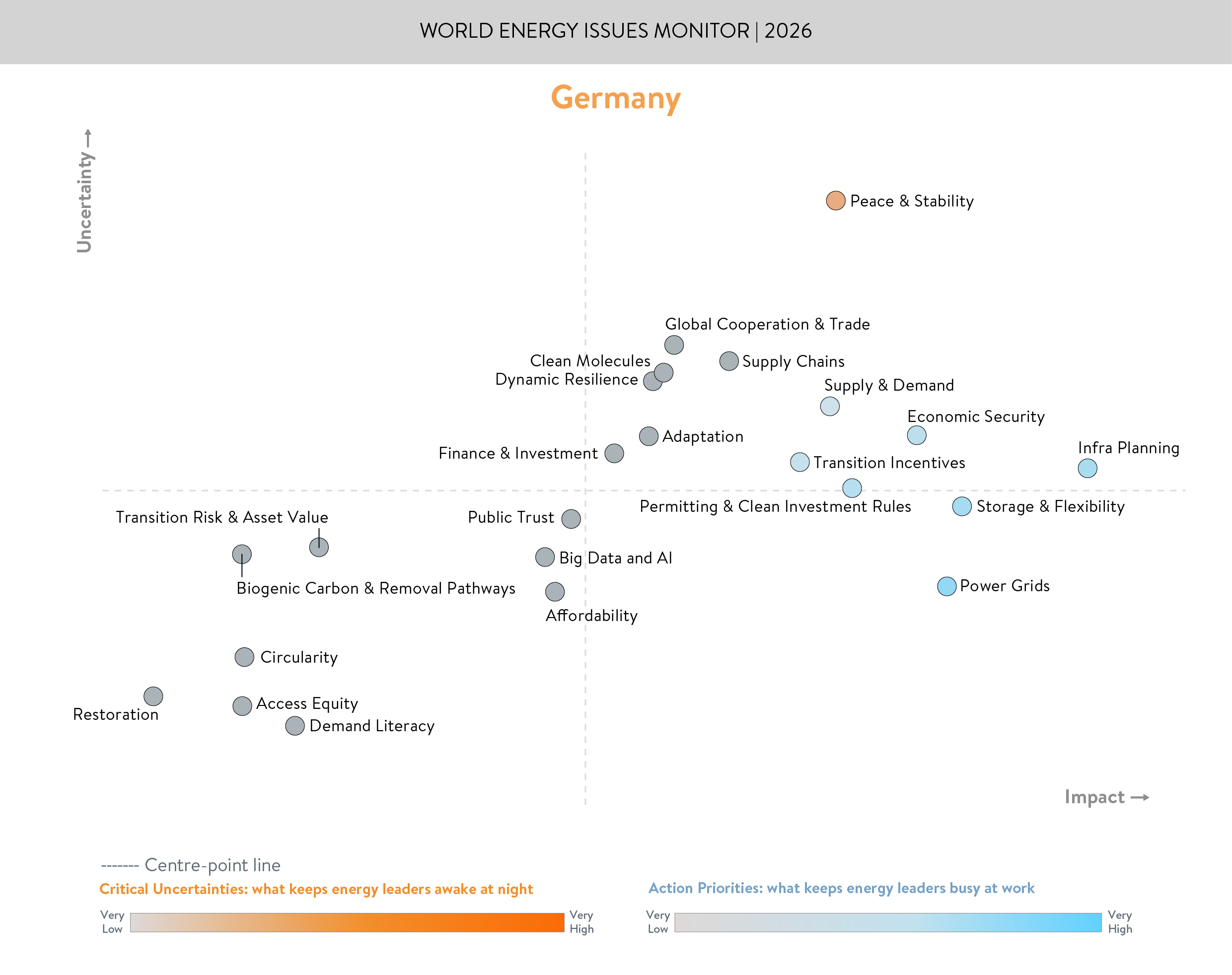

Germany's energy system entered 2025 navigating a geopolitical environment that has fundamentally redrawn the rules of energy security. That Peace & Stability tops the uncertainty scale not only in Germany but across Europe and globally is the defining signal of this year's Issues Monitor – a theme that, compared to 2024, has grown even more isolated on the map, sitting further from the cluster of other issues than in the previous year. Energy policy has always operated within a broader geopolitical context, but the current moment makes that relationship impossible to ignore. On global energy markets, energy policy is increasingly inseparable from geopolitical fracture lines: who supplies whom, on what terms, and with what leverage. In that sense, energy policy is security policy and, to some degree, peace policy. This is reflected in the ongoing consequences of geopolitical tensions: the continuing war in Ukraine and the US intervention in Venezuela. Events in the Middle East unfolded after the survey was conducted and are not yet captured in this year's results.

For Germany, this carries particular weight. The country remains structurally import-dependent: in 2025, imports accounted for 98% of mineral oil, 95% of natural gas, and 100% of hard coal. The net energy import bill stood at €74.5 billion, 76% above its 2020 level, making the cost of geopolitical exposure directly legible in the national accounts.

Affordability sits low on Germany's Monitor, not because costs are irrelevant, but because the past years have fundamentally recalibrated what energy is supposed to cost. The higher costs of LNG, diversified supply chains, storage capacity and grid redundancy are increasingly accepted as the price of a more resilient system. Resilience has a price tag, and the positioning of Affordability in this year's Monitor reflects that shift. This is one of the most striking changes compared to 2024, when Affordability appeared as one of the top-ranked critical uncertainties. Its migration to the lower half of the map suggests a meaningful shift in how German energy leaders are weighing cost against security.

A central finding of the 2025 Monitor is a qualitative change in the nature of Germany's action priorities. Infrastructure Planning, Storage & Flexibility, Power Grids and Economic Security all sit far to the right on the impact axis, but below the midline on uncertainty. Respondents see these as clear, high-impact priorities where the direction of travel is known. The challenge is not strategic orientation but execution. Germany now has 284 GW of installed generation capacity, of which 74% is renewable, yet renewables account for 58% of actual electricity generation. The gap between installed capacity and delivered output is precisely the integration challenge: grids, storage and flexibility mechanisms that can turn available capacity into reliable supply. This systemic framing is also visible in the positioning of Transition Incentives and Supply & Demand as action priorities on the German map, signalling that respondents see market design and incentive structures as practical delivery questions rather than open strategic debates.

Particularly notable is the positioning of Clean Molecules in the German Monitor. While this theme registers significantly lower priority among both European and global respondents, it appears as a clear action priority in Germany, reflecting a deliberate industrial policy choice that is not yet broadly shared across the international energy community. Germany is positioning hydrogen as the systemic answer to decarbonising processes that cannot be electrified: steel, chemicals, cement, as well as heavy transport, shipping and aviation. DNV projects Germany's hydrogen demand to increase sixfold to 7.1 million tonnes annually by 2050, lending long-term weight to the infrastructure decisions already being taken. With the approved hydrogen core network of 9,040 km and planned investment of €18.9 billion through 2032, Germany has already committed at scale, though implementation is only just beginning. A first concrete example is the GET H2 Nukleus project: a 130 km pipeline network from Lingen to Gelsenkirchen connecting electrolysers, cavern storage and industrial offtakers including steel plants in Duisburg and Salzgitter. In Brunsbüttel, the existing LNG terminal is planning ammonia imports from 2026 and a gradual conversion to a hydrogen import terminal, a direct bridge between short-term supply security and long-term decarbonisation strategy and an illustration of how Supply Chains and Clean Molecules are increasingly thought of together in German energy policy.

What the 2026 Monitor makes clear is that Germany's energy transition is no longer a question of ambition – it is a test of execution, resilience and the ability to hold the trilemma together under pressure.

Acknowledgement:

Germany Member Committee: Anna Molchanova, Dr Carsten Rolle, Prof. Dr Hans-Wilhelm Schiffer, Burkhard von Kienitz and Maira Kusch

Downloads

Germany World Energy Issues Monitor 2026 Country Commentary

Download PDF

World Energy Issues Monitor 2026

Download PDF

Germany World Energy Issues Monitor 2025 Country Commentary

Download PDF

World Energy Issues Monitor 2025

Download PDF

Germany World Energy Trilemma Country Profile 2024

Download PDF

World Energy Trilemma Report 2024

Download PDF

Related Publications

Innovation Insights Brief - New Hydrogen Economy - Hype or Hope?

Published on 04 June 2019

Innovation Insights Brief - Global Energy Scenarios Comparison Review

Published on 10 April 2019

World Energy Issues Monitor 2021: Humanising Energy

Published on 17 March 2021