ASIA NETWORK

The Asia regional network currently spans from New Zealand in the East, includes major economies such as Japan and China, and reaches India, Sri Lanka, and Pakistan in the South East. It is a large and diverse network in terms of its economic stages, culture, and language as well as energy issues it faces.

Key issues for the Asia region currently include accelerating the pace of transition to carbon neutrality, mitigating the risks associated with digitalisation and implementing new market design mechanisms. Recently, hydrogen has moved to the forefront of the discussion in many Asian countries as a potential way to decarbonise.

Regional action priorities that support the Council’s mission and humanising energy vision are agreed on an annual basis by national Member Committees in the framework of a Regional Action Plan. In 2021, Asian members joined forces to drive forward conversations on the future of hydrogen in the region.

Each month, the Asian regional network meets to discuss matters of mutual interest, drive collective activities, and keep each other updated on relevant developments and events. In addition, throughout the year regionally targeted workshops are being organised to advance discussions in the context of our global insights and innovation tools.

To drive action and achieve impact, members in the region work in partnerships with energy-related non-governmental agencies and other regional energy organisations including the Asian Development Bank (ADB), the Asian Infrastructure Investment Bank (AIIB), Asia Pacific Economic Cooperation (APEC), the Asia Pacific Energy Research Centre (APERC), the Institute of Energy Economics, Japan (IEEJ) and the Association of Southeast Asian Nations (ASEAN).

Conversations on hydrogen brought together stakeholders from the region and beyond.

A first webinar The Future for Hydrogen in the Asia Pacific was led by the Japanese Member Committee and explored the different drivers for hydrogen demand and emerging national hydrogen strategies, drawing on key findings from a recent Council survey.

A second webinar was co-hosted by the World Energy Council Hong Kong, WBCSD and ERM under the theme of The Emerging Hydrogen Economy in the Asia Pacific Region. The discussion built on the Council’s Innovation Insights Briefing Hydrogen on the Horizon: Ready, Almost Set, Go? and focused on different hydrogen strategies and action priorities in the Asia Pacific region and used.

Energy in Asia

INTRODUCTION

Asia’s Regional Commentary builds on insights surfaced through this year’s World Energy Issues Monitor dialogues, reflecting what leaders across the region said – not just what the survey shows. The survey and dialogues were conducted prior to the ongoing situation in the Middle East and therefore reflect conditions at that point in time.

Asia’s transition is anchored in structural growth, deepening electrification, and a pragmatic delivery mindset, yet increasingly shaped by global uncertainty. Ambition remains high, but recent experience has sharpened the primacy of security, affordability, and resilience. Geopolitical shifts, supply chain fragility, and uneven global trade are amplifying adaptation challenges. Unsurprisingly, coordinated infrastructure planning – especially around power grids, storage, and demand management – sits at the top of regional concern.

Across this landscape, reliability and decarbonisation remain core priorities. EV deployment is accelerating sharply and reframed as both load and flexible storage, while Australia’s home battery boom has accelerated demand side flexibility. Nuclear has re-entered the conversation, from Malaysia’s future mix considerations to China’s planning horizon. Beneath this, shifts on both the supply and demand side are giving rise to new business models, commercial arrangements, and operational practices – from prosumer driven flexibility and aggregation models to new service based approaches to storage, efficiency, and digital infrastructure. Affordability pressures and the need to actively build social licence continue to shape delivery.

Asia’s transition is also becoming more visibly system-bound as systems expand and transform simultaneously. Distribution networks, microgrids, and behind-the-meter assets are moving to the centre of planning; interoperability of distributed energy resources (DERs) is emerging as a constraint as some manufacturers shift toward proprietary systems, requiring government policies to keep pace with the market. High solar markets are experiencing midday negative wholesale prices, pulling storage and flexibility to the forefront and underlining the need for smarter tariffs or balancing storage and generation rollout. Cybersecurity is now a multidimensional risk – operational, financial, and geopolitical – as digitalisation expands. These changes demand greater adaptability from businesses, new technical skills across the workforce, and policy frameworks able to evolve at the pace of market and technological change.

These macro observations are reflected in this year’s Issues Monitor results: Asia moved storage & flexibility and power grids from “critical uncertainty” to “action priority,” while elevating adaptation, supply chain robustness, circularity, and policy clarity as key unknowns. The message is unmistakable: constraints are increasingly systemic – interoperability, grid readiness, workforce capability, supportive regulatory frameworks, investment confidence, cyber preparedness, and social licence – rather than a lack of technology. Under these tighter conditions, the leadership task is World Energy Trilemma-tested delivery: sustaining climate ambition while holding security and affordability in real time. The imperative is to protect what works while modernising delivery so the region can scale clean energy with resilience, and equip institutions, policies, and people to respond to a rapidly changing system.

|

ABOUT THE WORLD ENERGY ISSUES MONITOR Energy transitions are complex, evolving, and deeply interconnected, shaped by shifting priorities, emerging uncertainties, and regional realities. Since 2009, the World Energy Issues Monitor has offered a unique lens into the dynamic forces driving energy transitions worldwide. This year’s survey spans 23 core transition issues across six categories – spotlighting blind spots, new signals, and shifting leadership priorities. Amid growing uncertainty, leaders across the World Energy Council community are asking sharper questions: What’s working? What can be adapted across regions? And where are the real opportunities to turn blind spots into bright spots?

NOTE ON TIMING AND CONTEXT The survey and dialogues were conducted prior to the ongoing situation in the Middle East and therefore reflect conditions at that point in time. |

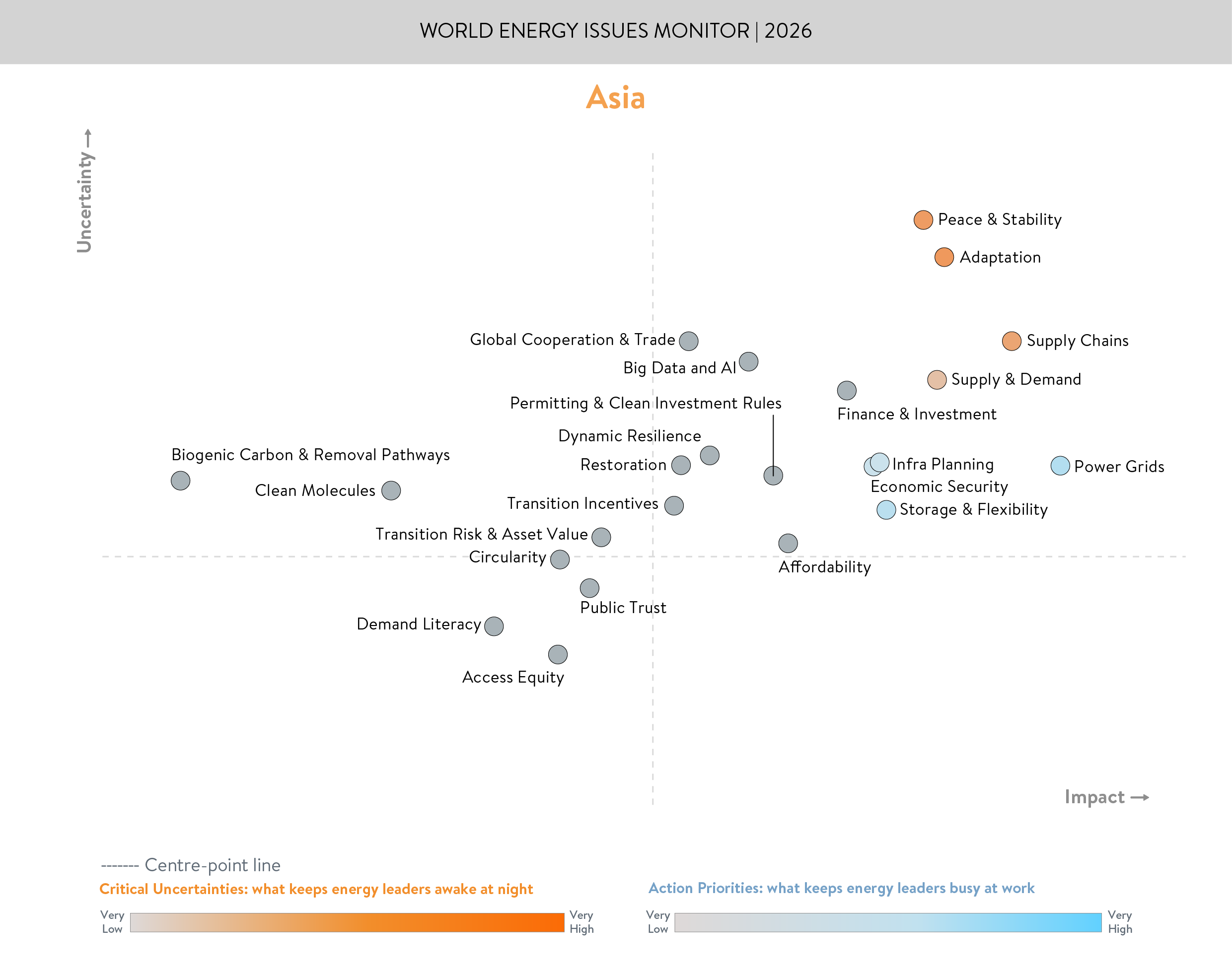

CRITICAL UNCERTAINTIES AND ACTION PRIORITIES

Top Critical Uncertainty: Peace and Stability

Peace and stability has become Asia’s defining operating condition – shaping investment horizons, energy‑system planning, and the region’s ability to navigate simultaneous transitions in security, climate, and industrial development. The uncertainty is no longer whether geopolitical disruption will occur, but how Asia can adapt under conditions of rising strategic competition, intensifying climate impacts, and increasingly contested global trade rules. Across the region, these pressures are now interacting with one another, exposing delivery systems to volatility in ways that directly influence cost, pace, and market confidence. In many markets, the speed of digitalisation and electrification is outpacing the ability of policy frameworks, regulatory systems, and workforce capabilities to adjust and respond at the necessary pace.

The 2026 Issues Map reflects this shift: perceived impact rises sharply across Peace & Stability, Global Cooperation & Trade, and Adaptation & Resilience, with more respondents placing these in the High/Very High Impact category. Uncertainty also increases for Peace & Stability and for global climate cooperation, underscoring the sense that Asia’s operating environment is being shaped by external pressures it cannot fully control, but must increasingly plan and invest around – including ensuring that skills, business models, policy, and planning frameworks evolve with the pace of system transformation.

Top Action Priority: The Delivery Spine – Grids + Flexibility + Planning

Asia’s transition is now constrained less by technology potential than by delivery throughput – where grids, flexibility, and coordinated planning set the real pace. The region’s rising digital loads, rapid electrification, and expanding prosumer base are placing unprecedented pressure on infrastructure readiness, regulatory clarity, investment conditions, and social license. These delivery enablers must now support security, affordability, competitiveness, and decarbonisation at the same time, under far greater scale and speed than previous build‑out cycles.

- Integrated grid and infrastructure planning is the pacing factor: Asia’s ability to scale renewables, electrification, AI‑driven demand, and industrial growth depends on integrated transmission and distribution planning that treats DERs and large new loads explicitly. While this is an opportunity for fast actors in the market, policy settings are lagging. Further, data centres, manufacturing hubs, and transport clusters require connection capacity and long‑lead‑time components that can’t be added piecemeal. The real constraint is shifting from what can be built to what can be connected and operated reliably, making coordinated planning essential to prevent congestion, curtailment, and rising system costs.

- Demand management and flexibility must be treated as system functions, not pilots: Demand management now needs equal footing with supply expansion. Flexibility – home batteries, VPPs, demand response, smart EV charging, V2G – is becoming core system infrastructure as consumers seek greener, time‑specific, and cost‑efficient energy. Peer to peer trading systems is an emerging market innovation. While, embedding flexibility near load reduces peak stress, volatility, and total system costs. Without it, high‑renewables grids risk deeper curtailment, higher balancing costs, and weakened public confidence.

- Grid infrastructure resilience is central to delivery credibility: Transmission and distribution resilience – capacity, redundancy, interconnection, protection – is becoming decisive for project timelines and investor confidence. Connection queues, long‑lead‑time hardware, and uneven regional grid strength limit where clean‑energy projects and new industrial loads can go. Strengthening resilience also means integrating DER contributions to system strength and inertia. As climate shocks and digitalisation accelerate, the grid’s ability to operate reliably under stress becomes the core test of transition credibility.

BLIND SPOTS AND BRIGHT SPOTS

Asia continues to scale renewables, but the 2026 picture is increasingly shaped by system constraints and legitimacy conditions that often remain secondary until they slow delivery. The Asia Issues Map and regional discussions point to a similar stress point: transitions are moving faster than the foundations can comfortably support.

Blind Spots

-

Access equity as the hidden determinant of connected progress: Despite being one of the most underestimated issues on the map, access equity is deeply intertwined with siting, permitting, and approvals. When early engagement is weak or uneven – especially in rapidly developing or vulnerable communities – legitimacy erodes, slowing project timelines and elevating local resistance. In a region with fast‑moving infrastructure growth, uneven access and participation can quietly become a systemic drag on delivery.

-

Demand literacy: a foundational, yet missing, capability: While demand is rapidly reshaping system dynamics – driven by AI, data centre growth, EVs, and rising electrification – regional literacy about how demand behaves and how it can be shaped is underestimated. Without shared understanding across policymakers, industry, and consumers, demand‑side flexibility will remain underutilised, and planning will lag reality. The risk is a persistent mismatch between where demand grows and how systems prepare for it.

-

Circularity and end‑of‑life systems remain a blind spot: Adaptation to climate shocks is emerging as a visible uncertainty across Asia, yet circularity in clean-energy systems remains largely peripheral in policy and planning. As deployment for solar, batteries, and wind accelerates, end‑of‑life volumes will scale non‑linearly. Without early integration of recycling, recovery, and reuse into energy strategies, the region risks a parallel vulnerability: mounting technology waste and new mineral‑supply constraints. The system is preparing for climate impacts while overlooking how insufficient circular infrastructure could itself constrain transitions.

-

Public trust: a strategic asset, not a stakeholder exercise: Public trust remains undervalued, yet it is fundamental to both transition speed and siting legitimacy. Community engagement and energy literacy are not keeping pace with the scale of development, and policy frameworks have not fully adapted to support consent‑building. Treating transitions as a common public good – not the remit of a small set of organisations – is essential to sustaining consent under rising cost, land‑use, and infrastructure pressures.

Bright Spots

-

Australia: Stabilising High VRE into system orchestration: South Australia operates with one of the world’s highest renewable energy grids while preparing for accelerated load growth and meeting the test of security challenges. Across the National Electricity Market, initiatives to increase both large-scale and home-scale storage including its national home battery rebate scheme. Australia has overtaken the United Kingdom in utility-scale battery capacity, with 37 GWh of projects at or nearing financial close, strengthening flexibility as new loads emerge.

-

China: Scale as a security strategy: In 2025 China added around 430 GW of new wind and solar, marking a 22% year on year increase, and pushing annual renewable capacity to about 4,000 TWh. New type energy storage including approximately 20 million EVs surpassed 100 GW, reinforcing the grid connected by ultrahigh voltage transmission. Smart siting strategies are seeing data centre development following available regional energy supply.

-

India: Record solar deployment with rising reliability focus: India installed roughly 37.9 GW of solar in 2025 – the highest on record – with rooftop additions of about 7.1 GW driven predominantly by households under the PM Surya Ghar scheme. Total renewable additions exceeded 40 GW, contributing to a rare full year decline in coal generation and reinforcing daytime reliability, even as grid and storage needs remain significant across states.

CONCLUSION

The events and signals emerging throughout 2025 reinforced a clear reality for Asia: transitions are not unfolding as a linear programme, but as system navigation under compounding pressure – where geopolitics shapes adaptation choices, rising demand reshapes system design, and legitimacy conditions shape what can advance at pace. The 2026 Asia Energy Issues Monitor reflects this backdrop: uncertainty is structural, system pressures are higher, and areas of progress and fragility now sit side by side across a rapidly diversifying region.

Four signals stand out:

-

Peace & Stability has hardened into the dominant uncertainty, shaping investment horizons and system planning as geopolitical tensions, climate impacts, and global trade shifts converge across Asia’s operating space.

-

Delivery throughput sets the pace: integrated grid planning, flexibility, demand side capability, and infrastructure resilience are now the backbone determining how quickly the region can scale renewables, meet new loads, and maintain reliability

-

Access equity and public trust are becoming decisive legitimacy conditions, influencing siting, approvals, and local participation – quietly determining where projects succeed or stall.

-

Adaptation is treated as a critical uncertainty while circularity remains undervalued, leaving a growing blind spot as end-of-life systems lag the pace of deployment and risk constraining transition from within.

Download the full report below.

KEY CONTRIBUTORS:

The Asia commentary draws on insights from across the World Energy Council community, and we are grateful to those who shared perspectives and challenge points that helped sharpen this year’s framing. We would particularly like to thank all of our Member Committees throughout Asia, in addition to the following organisations who have gone above and beyond in providing insights: China Electricity Council (CEC), State Grid Corporation of China (SGCC) , China Southern Power Grid (CSG), China Petroleum and Chemical Industry Federation (CPCIF), Sembcorp Industries, and Sarawak Energy.

Downloads

World Energy Issues Monitor 2026 - Asia Regional Commentary

Download PDF

World Energy Issues Monitor 2026 (Chinese Translation)

Download PDF

World Energy Issues Monitor 2026

Download PDF

World Energy Issues Monitor 2025 - Asia Regional Commentary

Download PDF

World Energy Issues Monitor 2025

Download PDF

World Energy Issues Monitor 2025 - Asia Regional Commentary (Chinese Translation)

Download PDFDownloads

Renewable Energy Systems Integration in Asia - Full Report

Download the Report

Renewable Energy Systems Integration in Asia - Executive Summary

Download the Executive Summary

Latest Publications

World Energy Issues Monitor 2026 - What Country Commentaries are Telling Us

Published on 24 June 2026

Practicing Trilemma Discipline – Regional Leadership Exchanges Highlights

Published on 16 June 2026

AI, Data Centres and the Future of Demand – WE Café Discussion Highlights

Published on 16 June 2026

Latest News