Latin America & The Caribbean Network

The Latin American regional network spans from Panama, Ecuador and Colombia in the North to Chile, Uruguay, and Argentina in the South, and includes further countries in central Latin America countries. The extensive network brings together the energy plus community in the region, including Ministers and government officials, CEOs, academics, energy experts, and young energy professionals to discuss and work for a sustainable energy future in the region.

Through events at regional and national level, the development of region-specific content and analysis, an extensive cross-border capacity building programme and collaboration with regional organizations such as the Development Bank of Latin America (CAF), Inter-American Development Bank (“IDB”) and Regional Energetic Integration Commission (CIER), national Member Committees work together to advance energy transition in Latin America and the Caribbean.

Regional action priorities that support the Council’s mission and humanising energy vision are agreed on an annual basis by national Member Committees in the framework of a Regional Action Plan. In 2021, Latin American members agreed to drive forward conversations on the future of hydrogen in the region, extend the reach of “We are all Energy” public awareness campaign across the region, and empower and connect young professionals to take an active role in the regional network.

Each month, the Latin American regional network meets to discuss matters of mutual interest, drive collective activities, and keep each other updated on relevant developments and events. In addition, throughout the year regionally targeted workshops are being organised to advance discussions in the context of our global insights and innovation tools.

Building on the 2020 interest of national Member Committees in the region and a Hydrogen Innovation Forum conducted, members in the region took forward the conversation on clean hydrogen as a promising solution to decarbonise hard to abate sectors such as industry and mobility while providing a seasonal storage solution. Key stakeholders engaged in discussions focussed on demand drivers and economics of hydrogen production and use as well as value chain developments, policy enablers and bottlenecks.

Initiated by the national Member Committee in Chile and the Chilean Agency of Energy Sustainability the “We are all Energy” campaign invites citizens to reflect on how energy, in all its forms, impacts people's life. Through a series of conversations supported by a social media campaign, “We are all Energy” raises public awareness about the role of energy as a key enabler to social and economic development, and the importance of advancing energy transition that leaves no one behind – now and for future generations. The initiative was extended to Argentina and Colombia who shared their local experiences and reflections around humanising energy transition.

Capacity building of professionals in the region has been a priority for national Member Committees for many years. World Energy Academy, a format initiated by the national Member Committee in Argentina (CACME) in 2014, provides professionals from different backgrounds with the tools to understand, assess and inform decisions, and exercise responsible leadership on energy issues. The World Energy Academy currently runs in Argentina, Bolivia, and Colombia.

National Member Committees across the region recognise the importance of empowering young professionals in the region to become actively engaged in and drive regional action priorities. Based on local vision and needs, Future Energy Leaders’ get involved through dedicated national programmes – in Panama, Chile, Argentina, and Uruguay – and / or in cross-border activities. At the same time, they have opportunity to network and interact with their peers and senior energy leaders.

Energy in Latin America and the Caribbean

INTRODUCTION

The Latin America and the Caribbean Regional Commentary builds on the insights uncovered in the annual World Energy Issues Monitor, weaving together the dialogue, tensions, and priorities emerging across the region. The survey and dialogues were conducted prior to the ongoing situation in the Middle East and therefore reflect conditions at that point in time.

Latin America and the Caribbean enters 2026 with strong transition advantages: abundant renewable resources, relatively clean electricity systems in several markets, growing relevance in critical minerals and clean fuels, and a compelling long-term narrative around low-carbon competitiveness. Yet the experience of recent years has clarified the limits of resource-led optimism when delivery is increasingly shaped by finance, infrastructure, institutional capacity, and political continuity.

Several 2025 signals reinforced this shift in the region’s operating environment. Climate shocks, fiscal pressure, and uneven institutional capacity tightened delivery conditions and exposed how quickly infrastructure fragility and financing constraints can escalate into system-level risks. At the same time, the region became more geopolitically exposed, as tensions around trade, strategic infrastructure, and foreign influence increased uncertainty over how energy, logistics, and industrial pathways will be shaped, and by whom.

Latin America and the Caribbean’s transition is also becoming more visibly “system-bound” in operational and political terms. The disruption of electricity exports from Colombia to Ecuador highlighted how interconnection alone does not guarantee security when political relationships are unstable. In parallel, grid constraints, planning delays, permitting, social licence to operate, and uneven regulatory continuity are making it harder to connect, move, and balance new supply at the pace required. Demand uncertainty is also sharpening, as digitalisation, industrial expansion, and new concentrated demand centres add pressure to systems already managing complexity with limited flexibility.

This is why Latin America and the Caribbean’s 2026 Issues Survey results emphasize this view: constraints are now systemic—rooted in finance and investment conditions, power grid readiness, supply and demand management, economic security, and institutional credibility—rather than a shortage of energy resources or transition opportunity.

Under these tighter conditions, the leadership task becomes a World Energy Trilemma-tested delivery: converting structural advantage into credible action while holding together security, affordability, and sustainability in real time, and building resilience in a more contested regional environment.

|

ABOUT THE WORLD ENERGY ISSUES MONITOR Energy transitions are complex, evolving, and deeply interconnected, shaped by shifting priorities, emerging uncertainties, and regional realities. Since 2009, the World Energy Issues Monitor has offered a unique lens into the dynamic forces driving energy transitions worldwide. This year’s survey spans 23 core transition issues across six categories – spotlighting blind spots, new signals, and shifting leadership priorities. Amid growing uncertainty, leaders across the World Energy Council community are asking sharper questions: What’s working? What can be adapted across regions? And where are the real opportunities to turn blind spots into bright spots? NOTE ON TIMING AND CONTEXT The survey and dialogues were conducted prior to the ongoing situation in the Middle East and therefore reflect conditions at that point in time. |

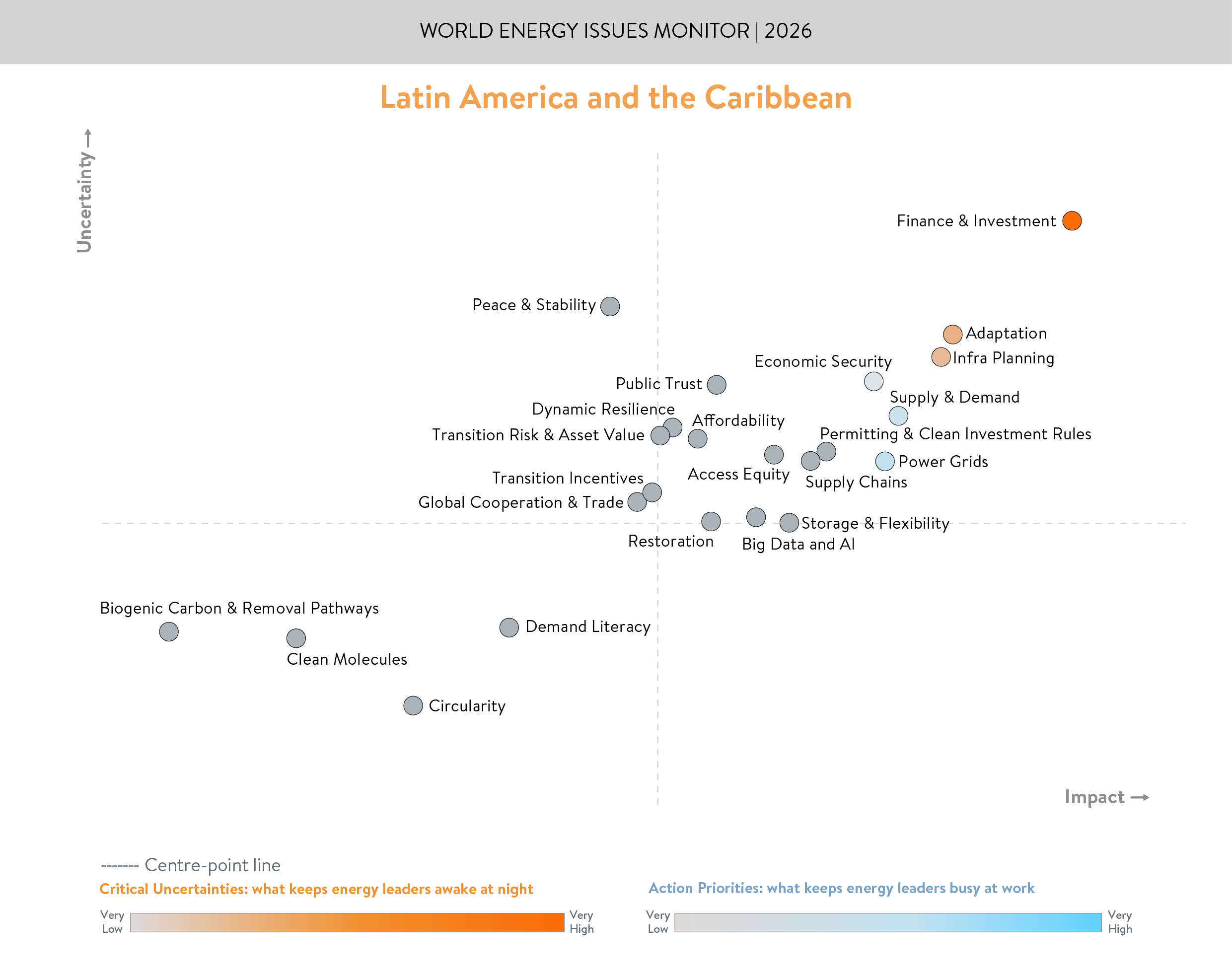

CRITICAL UNCERTAINTIES AND ACTION PRIORITIES

Top Critical Uncertainty: Finance & Investment

Finance & Investment has become Latin America and the Caribbean’s defining operating uncertainty, with Chile—and to a lesser extent Uruguay, Mexico, and Peru—standing out as partial exceptions. The central challenge is no longer the absence of opportunity, but whether the region can convert strengths in renewables, grids, storage, hydrogen, critical minerals, and emerging industrial value chains into projects that are financeable, scalable, and durable. This reflects wider concerns over high financing costs, uneven policy continuity, infrastructure bottlenecks, and weak coordination across energy, industry, and logistics planning.

One important source of this deterioration is the growing perception of U.S. interference in strategic projects across the region, named by the U.S. administration as the “Donroe' Doctrine”. U.S President’s Donald Trump's “200-year old plan for Latin America” applies especially where Chinese and Russian participation is significant. This includes interference affecting Venezuelan oil flows that supply China, U.S. opposition to the Chinese-controlled Port of Chancay in Peru on security and sovereignty grounds, scrutiny around the proposed transoceanic corridor linking Brazil to the Pacific with strong Chinese interest, and geopolitical positioning around Paraguay’s surplus Itaipu energy in the context of digital infrastructure and AI demand. Together, these cases point to a pattern in which external interference can influence investment conditions, infrastructure governance, and access to strategic assets. For the region, this raises uncertainty around sovereignty, planning autonomy, and the continuity of transition pathways tied to trade, energy, and industrial development.

Three dynamics that underpin Finance & Investment uncertainty stand out:

-

The cost of capital remains a central regional constraint. Strong resources and clear transition opportunities do not automatically convert into competitive delivery where financing costs remain high and risk-adjusted returns are difficult to secure.

-

Investment depends on credible long-term signals. Long-duration infrastructure and industrial projects require greater confidence in planning continuity, market design, and the consistency of public direction over time.

-

Bankability is increasingly tied to system readiness. Capital for generation, storage, digital demand, and industrial load growth is harder to unlock where transmission, permitting, and infrastructure coordination remain unresolved.

-

Adaptation is becoming part of the investment case. Climate exposure is increasingly shaping infrastructure assumptions, resilience needs, hydrological reliability, and the long-term viability of assets and systems.

Finance & Investment sits high on the regional uncertainty axis because it reflects the region’s ability to secure not only capital, but the political, institutional, and geopolitical conditions needed for investment, resilience, and productive development to move together.

Top Action Priority: The Delivery Spine — Grids + Supply and Demand + Economic Security

Energy security has returned to the top of the agenda in Latin America and the Caribbean as countries face a more fragmented and less predictable regional environment. A key driver is the weakening of political alignment across the region, which has made cross-border energy cooperation more fragile and less dependable. The recent interruption of Colombian electricity exports to Ecuador for political reasons illustrates how interconnection does not automatically translate into security when regional relationships are unstable. In this context, countries are placing greater emphasis on self-sufficiency, domestic reserve margins, and nationally controlled infrastructure, rather than relying on regional integration as the primary basis for resilience. This marks an important shift: energy security is no longer being understood mainly as a question of resource availability, but as a question of political trust, governability, and the reliability of external partners.

The issues Survey shows that Power Grids sits firmly as the leading action priority, while Supply & Demand and Economic Security reinforce the wider enabling delivery logic. The message these results suggest is that the region’s transition now depends on whether systems can absorb new supply, respond to changing demand patterns, and do so in ways that strengthen productive development and economic resilience rather than adding cost and fragility.

-

Grids are the pacing factor. Transmission and distribution constraints are increasingly determining how quickly renewable integration, electrification, and new industrial loads can advance. The binding question is not what can be built, but what can be connected, moved, and operated reliably, particularly under increased impact of extreme climate events and societal demand for more reliable supply.

-

Flexibility is becoming a core system requirement. Storage, digital optimisation, and demand-side management are increasingly necessary to support more variable and complex power systems. Without flexibility, higher-renewables systems face rising curtailment, volatility, and reduced delivery efficiency — weakening both affordability and transition credibility.

-

Supply and demand are becoming harder to manage through old planning assumptions. Industrial policy ambitions, digitalisation, and new concentrated demand centres are beginning to add pressure to systems that were not designed for this level of complexity. This is why planning quality and infrastructure sequencing are becoming as important as generation build-out itself.

-

Economic security is now part of the delivery logic. Energy infrastructure and system reliability increasingly shape competitiveness, productive development, and the credibility of national growth strategies. Where delivery conditions are weak, transitions risk being experienced less as engines of resilience and opportunity than as a source of additional cost and uncertainty.

BLINDSPOTS AND BRIGHT SPOTS

Latin America and the Caribbean continues to advance a strong transition agenda, but the 2026 picture is increasingly shaped by enabling conditions that often remain secondary until they affect delivery. The regional map shows a familiar tension: ambition is moving ahead faster than the system conditions needed to sustain implementation. The blind spots are therefore not areas of inaction, but areas where progress remains too partial, uneven, or weakly integrated, while the bright spots point to more practical, system-oriented transition thinking.

Blind Spots

-

Clean molecules may be facing a sequencing challenge rather than a loss of strategic relevance. Their lower salience points to the extent to which infrastructure, offtake, storage, and regulatory conditions still shape what can move from opportunity to delivery.

-

Adaptation is rising in importance, but resilience investment remains harder to finance. The challenge is less recognition than the ability to translate adaptation needs into investable delivery pathways.

-

Skills and talent pipelines may become more binding as systems grow more complex. The next phase of transition will require deeper technical, regulatory, and operational capabilities than many systems are currently building at scale.

-

Demand literacy may be weaker than the region’s next phase of planning will require. As industrial development, digitalisation, and new productive uses of energy expand, stronger visibility on where demand is emerging and how systems will need to respond becomes more important.

-

Social licence remains a practical delivery condition. Early engagement, community confidence, and public trust are becoming more decisive as transitions become more visible, territorial, and economically consequential.

Bright Spots

-

Brazil shows how structural advantage can be turned into productive strategy. Its relatively clean power base, large domestic market, and stronger industrial capabilities give it unusual leverage in the regional transition. Policy initiatives such as Nova Indústria Brasil signal an approach that links energy transition more directly to competitiveness, reindustrialisation, value creation, and green productive development, rather than treating decarbonisation as a standalone agenda.

-

Chile is emerging as a practical example of market and system-led transition thinking. Ongoing reforms and investment in storage, transmission, and grid management reflect a more mature recognition that transition success depends not only on adding renewable capacity, but also on managing congestion, improving flexibility, and strengthening overall delivery performance. This gives Chile a more operationally grounded transition profile, with greater attention to how systems function in practice.

-

Central America demonstrates that regional integration still holds practical value. The renewed momentum behind SIEPAC 2.0 — the upgraded phase of the Sistema de Interconexión Eléctrica para los Países de América Central(Electrical Interconnection System for the Countries of Central America) — suggests that interconnection and coordination remain among the clearest routes to greater resilience, efficiency, and system optimisation. In a more fragmented regional context, this stands out as an example of integration continuing to deliver practical system benefits.

CONCLUSION

The events and signals surfacing throughout 2025 reinforced that Latin America and the Caribbean is entering a more demanding phase of the energy transitions, one in which structural advantage matters, but no longer speaks for itself. The 2026 regional Energy Issues Monitor reflects this shift clearly. The region retains strong renewable resources, relatively clean electricity systems in several markets, and growing relevance in future energy value chains. But the pace and credibility of progress now depend increasingly on whether investability, system readiness, resilience, and productive development can move together.

Four signals stand out:

-

Finance & Investment has hardened into the region’s defining uncertainty, reflecting not a shortage of opportunity, but the challenge of turning opportunity into bankable, scalable, and investable delivery.

-

The delivery spine is becoming the practical test of transition progress, with grids, supply and demand management, and economic security increasingly determining whether systems can absorb new supply, respond to new forms of demand, and support competitiveness at the same time.

-

Climate exposure is moving into the core of the regional energy agenda, making resilience, adaptation, and infrastructure viability inseparable from questions of affordability, reliability, and long-term planning.

-

The next phase of progress will depend on how the region sequences its opportunities. Clean molecules, digital growth, regional integration, and system flexibility all remain relevant, but their practical value will depend on whether the enabling conditions around infrastructure, planning, skills, and public confidence can advance with greater coherence.

Across Latin America and the Caribbean, the challenge is no longer simply to expand transitions, but to sustain them under more complex delivery conditions. The agenda now is delivery over declarations: lowering the cost of moving from structural advantage to credible execution, strengthening the system foundations that support reliability and resilience, and ensuring that economic security is treated not as separate from transition, but as part of how it is made durable.

Download the full report below.

KEY CONTRIBUTORS:

The Latin America and the Caribbean commentary draws on insights from across the World Energy Council community, and we are grateful to those who shared perspectives and challenge points that helped sharpen this year’s framing, particularly Claudio Seebach, Felipe Barnal, Alexander Worner, Mariela Colombo, Chadia Abreu, Eduarda Zoghbi, Lucía Garín and Guadalupe Gonzalez.

Downloads

World Energy Issues Monitor 2026 - Latin America & The Caribbean Regional Commentary

Download PDF

World Energy Issues Monitor 2026

Download PDF

World Energy Issues Monitor 2025

Download PDF

World Energy Issues Monitor 2025 - Latin America & The Caribbean Regional Commentary

Download PDF

NATIONAL MEMBER COMMITTEES IN THIS REGION

Latest Publications

World Energy Issues Monitor 2026 - What Country Commentaries are Telling Us

Published on 24 June 2026

Practicing Trilemma Discipline – Regional Leadership Exchanges Highlights

Published on 16 June 2026

AI, Data Centres and the Future of Demand – WE Café Discussion Highlights

Published on 16 June 2026

Latest News