Europe Network

The European regional network currently spans 30+ countries, from Iceland and Ireland in the West to Russia, Kazakhstan, Armenia, and Turkey in the East, including most European Union member countries. The large and diverse European regional community provides national Member Committees and their members with excellent opportunities to expand and deepen their network and engage around activities and events – from young energy professionals to CEO and Ministerial level – to drive action and achieve impact.

Regional action priorities that support the Council’s mission and humanising energy vision are agreed on an annual basis by national Member Committees in the framework of a Regional Action Plan. In 2021, European members joined forces to work on the Insights Briefing ‘Decarbonised Hydrogen Imports into the European Union: Challenges and Opportunities’ and formed a working group to activate the Council’s Humanising Energy vision in the region.

Each month, the European regional network meets to discuss matters of mutual interest, drive collective activities, and keep each other updated on relevant developments and events. In addition, throughout the year regionally targeted workshops are being organised to advance discussions in the context of our global insights and innovation tools.

Hydrogen has the potential to become the second main energy vector after electricity for the decarbonisation of energy consumption in end-use sectors. Its role in deep decarbonisation scenarios has been increasing in recent years, together with dedicated roadmaps and strategies that have been published in several countries. Under the guidance of a Steering Committee consisting of several European member committees, a study was undertaken by the European Network into Decarbonised Hydrogen Imports into the European Union: Challenges and Opportunities.

The Insights Briefing explores possible scenarios for consumption and production of decarbonised hydrogen in the European Union, in line with its net-zero greenhouse gas emissions goals. Cost estimates for the production and transportation of decarbonised hydrogen from various power sources are presented for several European and neighbouring countries, out to the 2030- and 2050-time horizons.

To access the recent hydrogen study, please click here.

Several European members formed a working group to engage stakeholders in the Humanising Energy conversation to:

- Raise awareness of the human and societal dimensions of the energy transition

- Exchange views, experiences and best practices on relevant topics related to Humanising Energy

- Enhance visibility of the Council and its national Member Committees in the region around this topic

In July 2021, a side-event to the Vienna Energy Forum was organised, focusing on the challenges and opportunities of Humanising Energy in Regional Energy Transitions. Participants discussed how to fairly manage the impacts on regions and societies of faster paced energy transitions and looked at how stakeholders can work together in the process to effectively join the dots between ‘races to zero’ and social justice agendas.

As part of World Energy Week LIVE 2021, a conversation focusing on Active energy citizens: At the heart of the energy transition was convened. Participants explored how to ensure that all citizens, communities, and societies – including the most vulnerable – are involved in a clean and just energy transition.

Several countries in the region have developed national Future Energy Leaders Programmes. Periodically, events are organised to bring together the broad Future Energy Leaders community in Europe as well as European FEL-100 to network and engage in conversations around various energy topics. Webinars organised in 2021 include ‘How to Boost Renewables to Meet the EU Climate Target?’ and ‘The Future of Natural gas in the Energy System – a European Perspective’.

Energy in Europe

INTRODUCTION

The European Regional Commentary builds on the insights uncovered in the annual World Energy Issues Monitor, weaving together the rich dialogue shared by our community. The survey and dialogues were conducted prior to the ongoing situation in the Middle East and therefore reflect conditions at that point in time.

Europe’s energy transition remains anchored in long-term climate ambition and a deep clean-energy industrial base. Yet the experience of recent years has clarified the limits of ambition-led framing when delivery is increasingly shaped by security, affordability, and system capacity. In Europe, transitions are no longer unfolding as a linear programme; they are unfolding as system navigation under compounding pressure, where decision time is compressed and the cost of mis-sequencing is rising.

Several 2025 signals reinforced this shift in Europe’s operating environment. The end of Russian gas transit through Ukraine narrowed a once-familiar security margin and underscored how quickly supply conditions can change, even in systems built on interdependence. At the same time, affordability has moved from a background concern to a first-order political and industrial constraint – reflected in the EU’s Affordable Energy Action Plan, which positions competitiveness, security, and sustainability as inseparable requirements for the next phase of delivery.

Europe’s transition is also becoming more visibly “system-bound” in operational terms. The 28 April 2025 blackout affecting Spain and Portugal highlighted how quickly stability constraints can surface when systems run close to capacity – bringing grid resilience, system services, and flexibility to the centre of transition credibility. In parallel, demand uncertainty is sharpening: data centres and AI-related load growth are becoming material variables for planning, investment sequencing, and public consent – adding concentrated demand centres to an already widening set of electrification drivers. And as transition boundary expands across sectors, the start of Sustainable Aviation Fuel blending mandates in the EU and UK signals how policy is now creating new demand pull and investment expectations beyond the power system – linking decarbonisation to industrial scale-up and supply chain readiness.

This is why Europe’s 2026 Issues Survey results emphasize this view: constraints are now systemic – rooted in infrastructure readiness, regulatory predictability, investment frameworks, and social licence – rather than a shortage of solutions.

Under these tighter conditions, the leadership task becomes a World Energy Trilemma-tested delivery: sustaining climate ambition while holding together security, affordability, and sustainability in real time, and protecting what works while modernising what blocks delivery.

|

ABOUT THE WORLD ENERGY ISSUES MONITOR Energy transitions are complex, evolving, and deeply interconnected, shaped by shifting priorities, emerging uncertainties, and regional realities. Since 2009, the World Energy Issues Monitor has offered a unique lens into the dynamic forces driving energy transitions worldwide. This year’s survey spans 23 core transition issues across six categories – spotlighting blind spots, new signals, and shifting leadership priorities. Amid growing uncertainty, leaders across the World Energy Council community are asking sharper questions: What’s working? What can be adapted across regions? And where are the real opportunities to turn blind spots into bright spots?

NOTE ON TIMING AND CONTEXT The survey and dialogues were conducted prior to the ongoing situation in the Middle East and therefore reflect conditions at that point in time. |

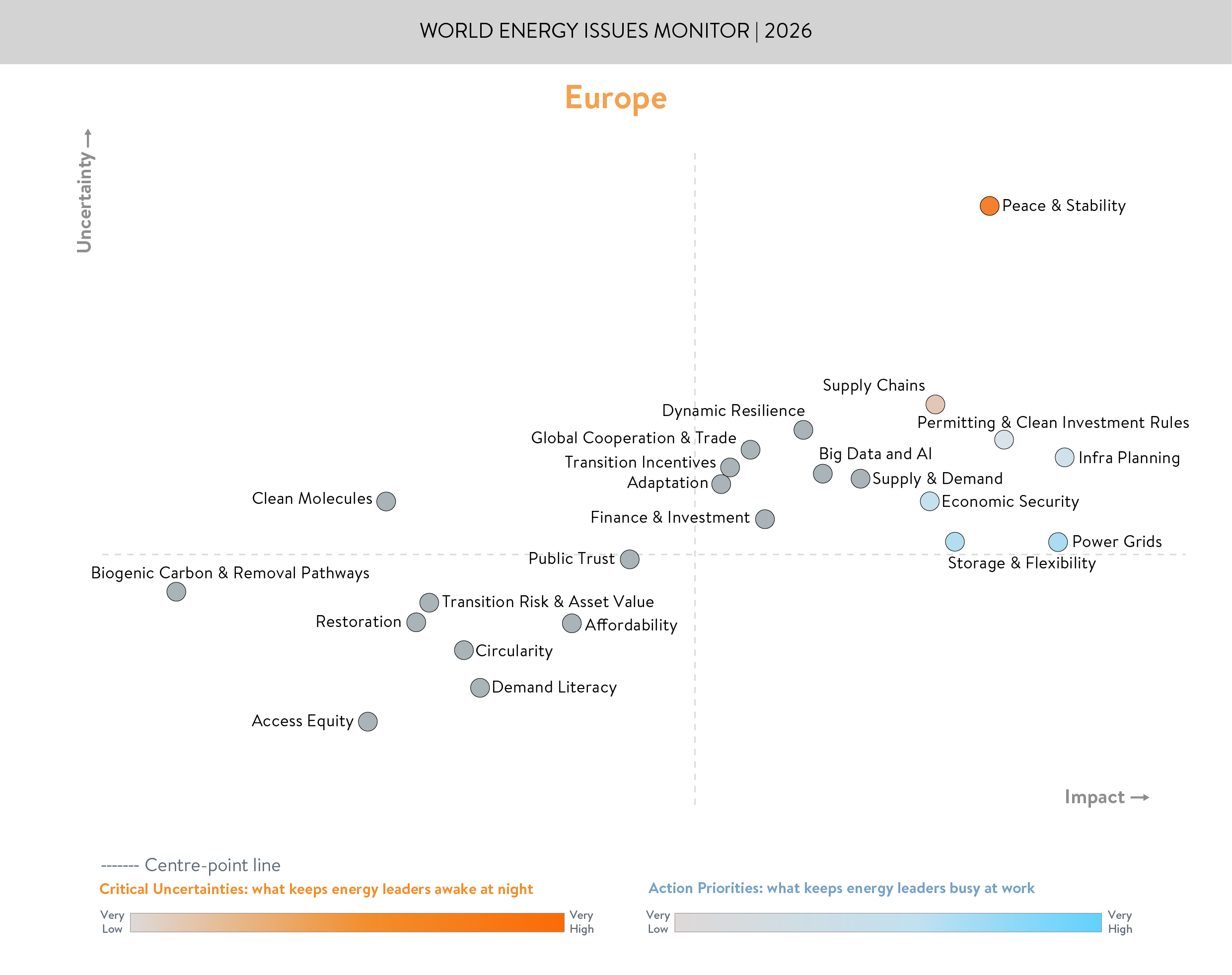

CRITICAL UNCERTAINTIES AND ACTION PRIORITIES

Top Critical Uncertainty: Peace and Stability

Peace and stability has become Europe’s defining operating condition – shaping investment horizons, industrial strategy, and market confidence. The uncertainty is less about whether disruption occurs, and more about how Europe navigates three compounding pressures: geopolitics as a market-shaper, rising trade fragmentation and contested standards, and climate impacts increasingly treated as operational security risks.

Three dynamics that underpin Peace & Stability uncertainty stand out:

-

Sovereign reliability is now a pricing factor: Europe’s energy and industrial choices are being shaped as much by alignment, resilience, and strategic dependencies as by economics. As geopolitical forces act as market-makers, they raise the cost of capital, compress decision time, and increase delivery risk – especially where supply chains, critical materials, and infrastructure sit within contested spheres of influence.

-

Security risks are converging: climate shocks, cyber exposure, and geopolitical volatility are increasingly bundled into a single risk picture for energy systems. This convergence is reshaping investment horizons and public confidence, and is accelerating demand for resilience-by-design across grids, infrastructure, and supply chains.

-

From fuel swapping to dependency reshuffling: diversification away from Russian pipeline gas has reduced one strategic vulnerability, but also reconfigured exposure to global LNG markets and supplier priorities. The result is not “energy sovereignty” in the traditional sense, but a new map of entanglements – where the nature of dependencies (and their political conditions) becomes as decisive as price.

Top Action Priority: The Delivery Spine – Grids + Flexibility + Planning

Europe’s transition is now constrained less by technology availability than by system throughput – with grids, flexibility, and planning setting the pace. Delivery constraints have become systemic: infrastructure readiness, regulatory predictability, investment conditions, workforce capacity, and social licence must now carry a heavier load, because they are expected to serve security, competitiveness, decarbonisation, and political viability simultaneously.

-

Grids are the pacing factor: network expansion, connection queues, and cross-border coordination increasingly determine how quickly renewables, electrification, and new industrial loads can scale. The binding question is no longer “what can be built”, but what can be connected and operated reliably.

-

Flexibility is inseparable from grid modernisation: storage, demand-side response, and dispatchable low-carbon capacity are becoming core infrastructure, not optional add-ons. Without flexibility, high-renewables systems face rising curtailment, volatility, and higher system costs – undermining both affordability and legitimacy.

-

Permitting and planning are throughput constraints: complexity and timeline risk in planning and approvals – alongside local acceptance and overarching regulatory complexity – can delay or reshape critical transmission and generation upgrades. Where regulatory efficiency is enabling and early engagement is done well, delivery friction can be minimized while strengthening social licence for continued build-out.

-

Affordability is a delivery input: high energy costs are not only an economic challenge but a legitimacy constraint. Policy is increasingly judged by whether it delivers visible cost relief and competitiveness, alongside decarbonisation – reflected in the EU’s Affordable Energy Action Plan and its emphasis on reducing costs while accelerating investment.

BLIND SPOTS AND BRIGHT SPOTS

Europe continues to scale renewables, but the 2026 picture is increasingly shaped by system constraints and social licence enablers that are often treated as secondary until they stall delivery. The Europe Issues Map and regional discussions point to a stress point: transitions are moving faster than the foundations – institutions, infrastructure, and public consent – can comfortably support.

Blind Spots

-

Market design credibility is becoming a stability risk: public and political questioning of marginal pricing and burden-sharing is rising. If mishandled, this can become a disruptive fault line – undermining investability, slowing grid build-out, and weakening the legitimacy needed for delivery.

-

Affordability is not a side issue – it is a structural constraint on delivery: affordability pressures in power, gas, and electricity are driven less by under‑investment in resilience or modernisation than by exposure to expensive gas and the accumulation of charges, levies, and taxes that disproportionately burden electricity compared to other energy carriers (as highlighted in the Draghi report). Prices must remain socially and industrially acceptable to sustain consent, even as systems require continued investment for resilience and modernisation.

-

Permitting and planning remain underestimated throughput constraints: despite being underrated on the map, approval timelines and local acceptance continue to decide what gets built, where, and how fast – especially for networks and new infrastructure. Planning must be proactive and early, and aligned with energy targets.

-

The “missing half” of system design: clean molecules strategy: the lagging cost efficacy compared to other sources is obscuring the build-out required for clean molecules (including hydrogen) for hard-to-abate sectors. The strategic pressure point is that Europe is building a dual system (electrons + molecules) while operating under legacy market rules – adding friction under time pressure and contested policy conditions.

Bright Spots

-

Spain: disruption as an accelerant for resilience: Spain is using system stress to accelerate the update of operating rules and procedures – moving beyond frameworks designed for early‑2000s systems toward rules fit for today’s high‑renewables reality. The experience reinforces that resilience is strengthened through adaptive governance and learning‑by‑doing, not only through advance planning.

-

France: strategic certainty as an investment signal: France is using long-horizon system planning and clarity on firm capacity to reinforce security and investability. Even as the mix evolves, the signal to markets is one of continuity and strategic intent.

-

Germany: renewables becoming structural: Germany’s progress reflects a broader shift: renewables are increasingly treated as core system infrastructure – supported by reforms that aim to reduce connection and curtailment friction and keep scaling aligned with grid reality.

CONCLUSION

The events and signals surfacing throughout 2025 reinforced a clear reality for Europe: transitions are not unfolding as a linear programme, but as system navigation under compounding pressure – where geopolitics shapes markets, affordability shapes legitimacy, and operational constraints shape what is feasible at pace. The 2026 Europe Energy Issues Monitor reflects this backdrop: uncertainty is structural, system pressures are higher, and progress and fragility now coexist in the same operating space.

Four signals stand out:

-

Peace & Stability has hardened into the dominant uncertainty, shaping investment horizons, industrial strategy, and confidence – through reconfigured dependencies, trade fragmentation, and the convergence of geopolitical, cyber, and climate risks.

-

Delivery throughput sets the pace: grids, flexibility, permitting, investability, and workforce capacity are no longer enabling “add-ons” but the delivery spine – determining how fast electrification, renewables, and new industrial loads can scale.

-

Affordability is a delivery input and a legitimacy constraint: transitions are increasingly judged by whether they deliver visible cost relief and competitiveness while sustaining investment in resilience and modernisation.

-

Market design credibility and trust are emerging as stability variables: contested pricing and burden-sharing debates can amplify uncertainty, weaken investability, and slow build-out if reforms do not land with public and industrial confidence.

Download the full report below.

KEY CONTRIBUTORS:

The Europe commentary draws on insights from across the World Energy Council community, and we are grateful to those who shared perspectives and challenge points that helped sharpen this year’s framing, particularly the Spanish Member Committee.

Downloads

World Energy Issues Monitor 2026 - Europe Regional Commentary

Download PDF

World Energy Issues Monitor 2026

Download PDF

World Energy Issues Monitor 2025

Download PDF

World Energy Issues Monitor 2025 - Europe Regional Commentary

Download PDF

Decarbonised hydrogen imports into the European Union: challenges and opportunities

Download PDF

Phasing Out Carbon - How to decarbonise North-Western Europe's energy mix in the run-up to 2050

Download PDF

Latest Publications

World Energy Issues Monitor 2026 - What Country Commentaries are Telling Us

Published on 24 June 2026

Practicing Trilemma Discipline – Regional Leadership Exchanges Highlights

Published on 16 June 2026

AI, Data Centres and the Future of Demand – WE Café Discussion Highlights

Published on 16 June 2026

Latest News